This round will see a new opportunity for the industry to propose projects with up to 10% of the capacity deemed to integrate a “qualifying innovation”. Although yet to be defined, we hope innovation may be applicable during any lifecycle stage and related to any part of the project to address an industry-wide problem (like noise due to pile driving during the installation), de-risk technology (e.g. turbine level energy storage) and/or boost UK benefit (e.g. journal bearings or concrete towers).

This is a great chance for new technology to have a stepping stone to commercial scale roll-out on an operational site. In many cases, the supply chain is not yet in a place to serially manufacture at the order of magnitude required for a large project. Including innovative features within a larger project brings the benefits of shared infrastructure and an opportunity for UK supply chain to invest in facilities ready to serve an ongoing pipeline of projects.

As further incentive, The Crown Estate will reduce seabed leasing charges by 50% on up to 10% of the project capacity for the first five years of operation for sites with a qualifying innovation, which could save wind farm operators in the order of £200,000 a year* to be used towards funding innovative technologies.

Floating wind is at the cusp of commercial success and a hybrid site (e.g. 10% floating foundations and 90% fixed) could be the final step to achieving acceptance as a mature, bankable technology. This type of arrangement could open up access to commercial funding arrangements and close the gap with bottom-fixed wind in competitive CfD auction rounds. A site with water depths in a range of 45m to 50m and above could use a combination of bottom-fixed foundations and semi-sub style floating foundation, or other designs which are suitable for the shallower end of floating wind water depths.

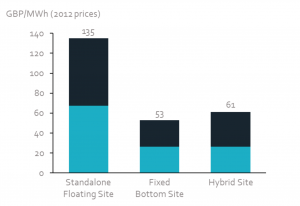

Our report “Macroeconomic Benefits of Floating Wind in the UK” estimates a standalone 96MW pre-commercial floating wind site to have an LCoE of £135 per MWh (2012 real) in 2025. However, the standalone floating site modelled in the Macroeconomic Benefits study is assumed to bear the full cost of infrastructure. In reality, around 50% of costs are common between fixed and floating turbine sites. The majority of development and operating costs, as well as grid connection, can be shared across the fixed and floating zones. The hybrid site also carries less financial risk and therefore attracts more favourable financing and insurance rates compared to a standalone floating site. If a floating project of that size were co-sited with a 1GW site, with its LCoE modelled at the cap strike price for projects coming online in 2025, £53 per MWh, the average LCoE across the site would be £61.20 per MWh. This is illustrated in Figure 1.

At this price, floating wind projects are a much more attractive proposition for investors and electricity consumers. Combined with other breakthrough technology aimed at reducing cost, such as advanced wind farm control and autonomous systems, the actual site-averaged LCoE could come in closer to the cap of £53 per MWh. This would make projects that include floating wind technology a step closer to being competitive with bottom-fixed sites for the first time.

*For a 1GW site operating at 50% capacity factor receiving £53 per MWh.