Today’s announcement of Allocation Round 6’s (AR6) administrative strike price (ASP) allows us to explore some potential outcomes to the upcoming auction round. Here our Analysis & Insights Manager, James Mantell, gives an initial overview:

The ASP has increased from £44/MWh to £73/MWh, the CfD uses 2012 prices. The increase in ASPs is poised to facilitate a more extensive deployment of offshore wind. Given the complexity of the Contracts for Difference (CfD) formula there are other important variables, which will not be released today, and therefore this analysis only shows how they may impact the auction round. This analysis also uses information from AR5 where no new information has been given regarding AR6 (load factors, etc.)

Below is a simplified formula for calculating the CfDs:

Budget impact = (Strike Price – Reference Price) X Load Factor X Capacity X (Days X 24)

With only the ASPs, we can illustrate outcomes using example reference prices. Reference prices are the estimated market price of electricity (by the government). In AR5 reference prices were set notably lower than market price forecasts. With these new ASPs there is trade-off between increasing reference prices and the impact on the budget or “pots”. Technologies are grouped into different pots. Pot 1 included fixed-bottom offshore wind, onshore wind, and solar, however going forward offshore wind will have its own Pot. The pot size in AR5 was revised to £190m.

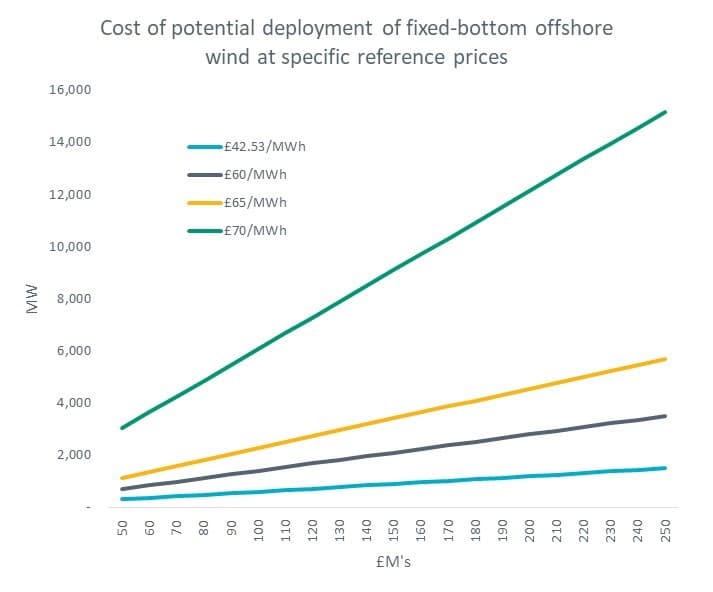

If the reference price and pot size remain unchanged from £43/MWh & £190m for AR6 2026/2027 (the first likely year of deployment), then the total potential deployment for offshore wind will be limited to approximately 1GW, as shown in Figure 1. At these 2023 reference prices A Pot size of roughly £500m would be needed to deploy 3GW of offshore wind. However it is likely the reference prices will increase, and below we look at this impact to the required budget size.

We can use these figures to understand what scale of deployment is needed to reach the Government’s 2030 targets of 50GW. There is currently 14.7GW of installed offshore wind capacity fully commissioned and approximately 12GW (Figure 2) either partially commissioned, being built, or with a CfD secured, giving us approximately 27GW in the pipeline. This means approximately 23GW needs to secure CfDs in AR6, AR7, AR8, and possible AR9 to be built by 2030. Figure 2 shows we need an additional 6GW to be secured per year in 2024, 2025, 2026, and 2027 on top of the already CFD-secured pipeline to reach the Government’s targets. This assumes it takes 3 years to complete a project from CfD award.

If the reference price increases to £60/MWh, then offshore wind would need approximately £430m of support through the AR6 CfD per year for the 6GW required.

If the reference price increase to £65/MWh then offshore wind would need approximately £260m of support through the AR6 CfD per year for the 6GW required.

And lastly, if reference prices increased to £70/MWh then offshore wind need approximately £50m of support through the AR6 CfD per year for the 6GW required.